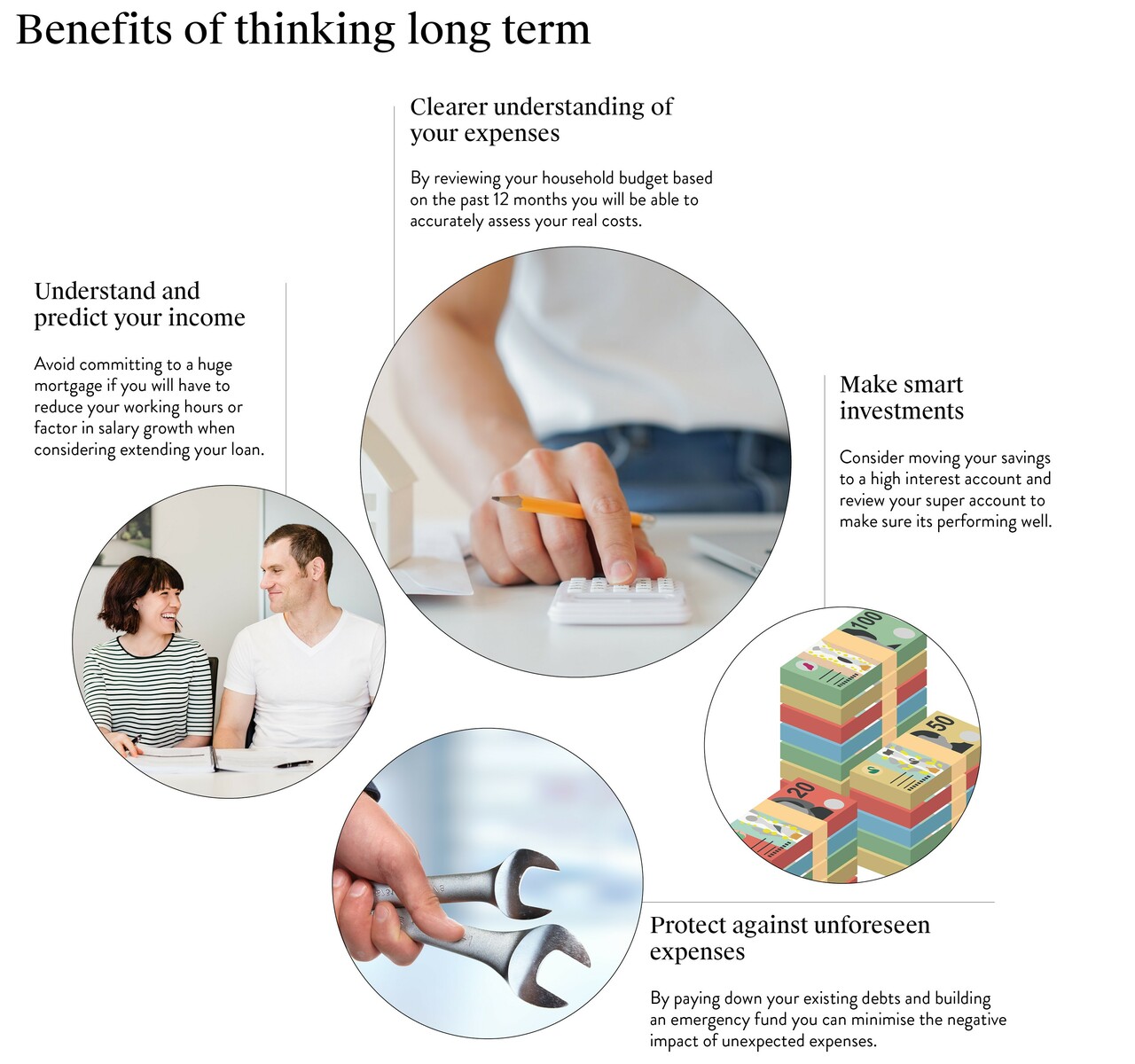

Simple ways to future-proof your finances

To get ahead, you must think beyond a paycheque-to-paycheque budget and start to make longer-term plans.

That means keeping an eye on the economy, thinking about your career over different life stages, and spotting opportunities as they arise. Most importantly, it means being prepared to adjust your financial plan when circumstances change.

Why is building a financial buffer so important?

Building a financial buffer is one of the most effective ways to protect your finances from unexpected shocks. A financial buffer, often referred to as an emergency fund, is money set aside to help cover unplanned expenses without disrupting your long-term financial plan.

Unexpected costs can arise at any stage of life. Household repairs, medical bills, car maintenance, or temporary income loss can quickly place pressure on your budget if you are not prepared. Without a buffer, many Australians are forced to rely on credit cards or personal loans, which can increase debt and add long-term financial stress.

A strong financial buffer helps smooth out these disruptions. By having accessible savings available, you can continue to meet regular expenses, maintain loan repayments, and avoid making rushed financial decisions during stressful periods. This level of preparation plays a key role in helping you future proof finances and maintain greater peace of mind.

As a general guide, many financial advisers recommend building a buffer that covers three to six months of essential living expenses. While that may feel ambitious, starting small and contributing regularly can still make a meaningful difference over time.

How can reducing debt and liabilities strengthen your future finances?

Reducing debt and ongoing liabilities can strengthen your financial position by freeing up cash flow and reducing long-term financial pressure. Some key benefits include:

- Lower monthly repayments, making your budget easier to manage

- Reduced exposure to interest rate increases

- More income available for savings and long-term goals

- Improved borrowing capacity when applying for a home loan

- Less reliance on credit cards and personal loans

- Greater flexibility during periods of income change

- Increased confidence when making major financial decisions

What long-term financial planning strategies can help you stay ahead of your expenses?

Long-term financial planning focuses on creating strategies that support stability and flexibility as your circumstances change. Some key approaches that can help you stay ahead include:

- Planning for income changes: Consider how your income may evolve over different life stages, including career growth, reduced hours, or changes in household income.

- Diversifying income where possible: Relying on a single income source can increase financial risk. Exploring additional income streams may help strengthen long-term security.

- Reviewing your financial plan regularly: Regular check-ins allow you to adjust goals, budgets, and strategies as economic conditions and personal priorities shift.

- Balancing short-term needs with long-term goals: Effective planning ensures you can manage day-to-day expenses while still working towards future milestones.

Planning in the long term isn’t just about predicting every outcome, but about being prepared for change. By reviewing your finances regularly and adjusting your plan as your income, goals, and life stages evolve, you can respond more confidently to shifts in the economy and protect your finances over time.

Why is professional financial guidance worth considering?

Professional financial guidance can help bring clarity to complex financial decisions, particularly when planning for the future. A financial adviser can offer personalised financial advice based on your goals, income, and life stages, helping you make informed choices with greater confidence.

Some key benefits of seeking financial guidance include:

- Support when making major financial decisions

- A clearer understanding of how different options may affect your future

- Help tailoring a financial plan to suit your lifestyle and goals

- Being able to look through government schemes that you may be eligible for

- Guidance through changing circumstances, such as career shifts or family changes

- Improved confidence when managing savings, debt, and investments

While professional advice is not essential for everyone, having access to expert guidance can help ensure your financial plan remains relevant and adaptable. It can also provide reassurance that your decisions are aligned with your long-term goals and financial future.

Ready to future-proof your finances and do some budgeting?

Future-proofing your financial position does not require drastic changes. By taking small, considered steps and reviewing your finances regularly, you can improve stability and prepare for the future with greater confidence. Whether you are saving for a home, managing debt, or planning for different life stages, a clear financial plan can help guide your next move. Contact us to get started in planning your dream home.