How Much Difference Does an Interest Rate Rise Make?

by Carlisle Homes

Here’s what you need to know about interest rate rises and how you can prepare.

On Tuesday 3 May, the Reserve Bank voted to raise interest rates for the first time since 2010. The rise is a modest 0.25, taking the cash rate to 0.35. However, the Reserve Bank governor, Philip Lowe, has all but guaranteed that borrowers can expect further rate hikes over the next couple of years.

What does that mean for borrowers in real terms? Maybe not as much as the headlines would have you fear. Here, we’ve broken down what each rate rise means for the average mortgage holder, and what you can cut back on to compensate.

What is the average loan size?

According to ABS figures released in January 2022, the average new mortgage size taken out in Victoria was $652,187. CoreLogic figures are similar, assuming a loan of $644,915 against the median property price of $806,144. We’ll be assuming a mortgage of $650,000 for the following scenarios, but of course, if you’ve had your loan for longer, or bought a less expensive home, your position will be better. For example, a Carlisle house and land packages start at just $540,800.

Your existing interest rate also factors in. In January 2022 (prior to the rate rise), ABS figures indicate an average rate of 2.52% per annum for new loans. We’ve taken that figure for our calculations.

Lower the impact of the interest rate rise by making some simple changes to your spending.

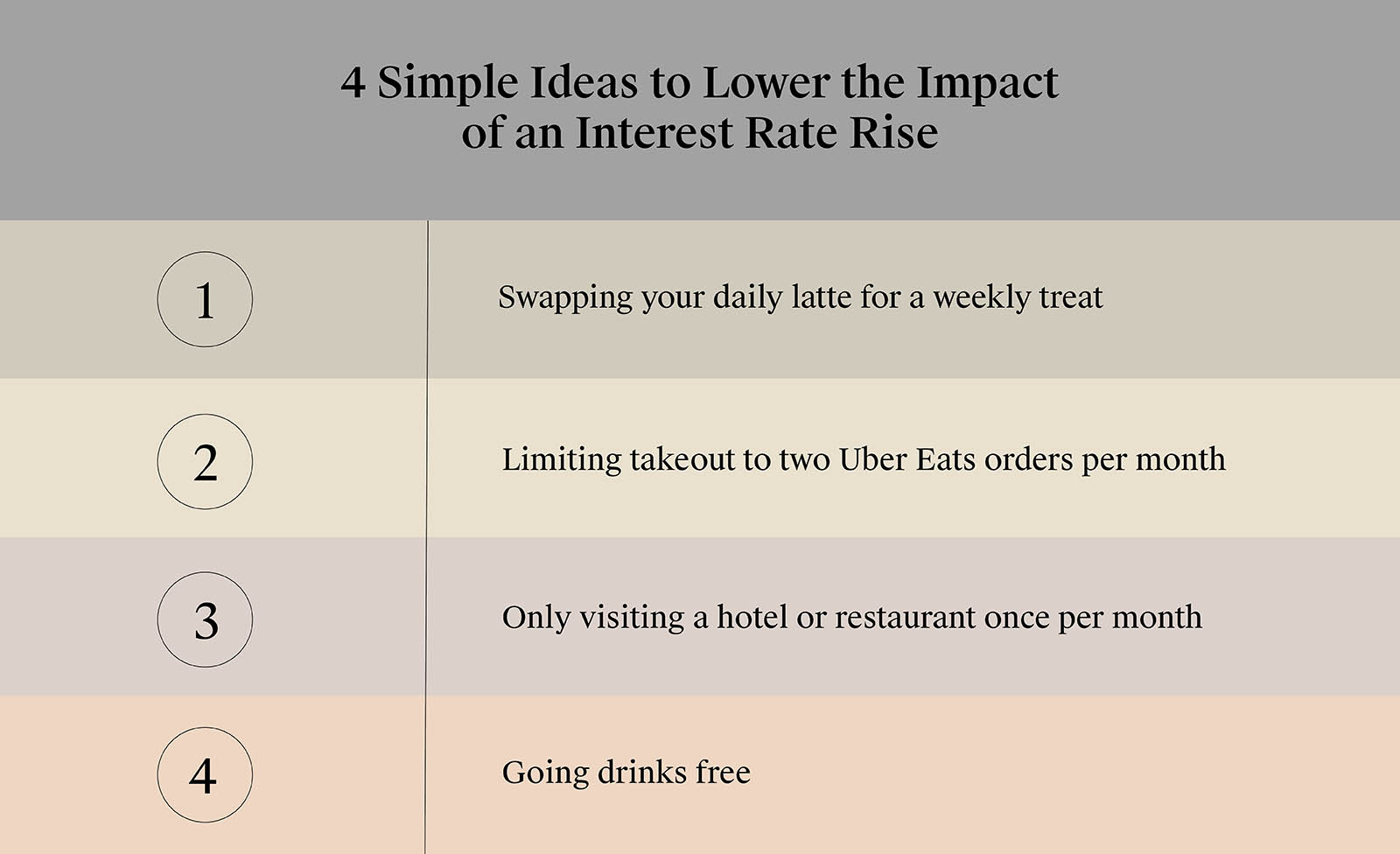

At the current cash rate of 0.35%, repayments on an average Victorian loan go from $2,575 per month to $2,660. That’s an increase of $85 a month or:

- Swapping your daily latte ($6/day or $120/month) for a weekly treat ($24/month)

- Two Uber Eats orders per month

- One visit to a hotel or restaurant per month

- Going drinks free: a saving of $22 per week for a single Australian under 35

Future rate rises

So far, so good. But what if rates keep going up?

If the cash rate hits 1.25% by January 2023, as predicted by the CBA, interest rates can be expected to rise to 2.67% - still extremely low by historical standards. In this scenario, the average loan repayment will rise to $2,980.82. That’s $405 more per month or:

- Half the amount we spend per month on recreation and culture ($191 per week)

- The same amount we spend on household furnishings per month ($103 per week)

- Two nights’ holiday in Melbourne for a domestic traveller

- An annual three week trip to the United States ($4500 or $375 per month)

Once you’ve figured out how you’ll compensate for interest rate rises, it’s worth devising a plan that you can activate if they keep going up. Featured here: Renwick, Kaduna Park Estate, Officer South.

What can you do now?

While rates may be going up, they’re unlikely to jump dramatically. The RBA doesn’t want to cause a shock to the system whereby Australians have to make drastic changes to their budget. Rather, they’re taking a slow and steady approach.

As a borrower, you can get ahead of the game by using this opportunity to do a budget health check. For example:

- Do you have any subscriptions you’re not using anymore? Streaming services, gym memberships and loyalty programs can all slip under the radar long after they’ve reached their use-by date.

- Are you getting the best deals on your insurance? There are many comparison websites and services that will help you check your health, home, car and life insurance policies to see if there are available savings to be had.

- ‘Clothes shop’ at home by doing a stocktake of your wardrobe and other cupboards. You may be surprised by what you already have, and come up with different ways to wear it.

- Develop thrifty habits, like bringing lunch and your morning coffee from home instead of buying it at expensive cafes. Find other ideas for saving money here.

- Consider whether you can you live with the phone you own now for another year or two saving on technology expenses.

- Delay the investment in big expenses such as cars or furnishings to get ahead in your mortgage savings, combatting the need to adjust quickly to rate rises.

And of course, check with your broker to see if your home loan is working hard for you. There are so many products on the market that there may be an opportunity to get a better deal on a variable or fixed-rate loan.

Avoid getting caught off guard with a budget health check! Re-evaluate all your financial commitments, big and small, to see whether they still contribute to your lifestyle.

Want to know more about current interest rates, budgeting and all things finance? Visit the Finance section of the Home Files for more professional guidance to assist you on your journey.